Among the “Market Neutral” strategies we find the Long Strangle Strategy. These are non-directional strategies where the trader does not know which way the price may go. The trader can profit if the price moves in either direction. This strategy is similar to the Long Straddle but with some differences.

- The Long Strangle strategy consists of buying an out-of-the-money call option and an out-of-the-money put option, both with the same expiration date.

- This strategy seeks to take advantage of an increase in the volatility of the underlying asset.

- It needs a strong movement in the underlying asset to bring profits by the expiration.

The main difference with the Long Straddle is the cost. The Long Strangle costs less because it uses two out-of-the-money strike prices. However, the Strangle requires a greater move because the strikes are further away.

This strategy can be used around a macro event or a catalyst. For example, the release of central bank statements such as monetary policies on interest rates or the release of quarterly results can be events that bring up the volatility of the underlying asset.

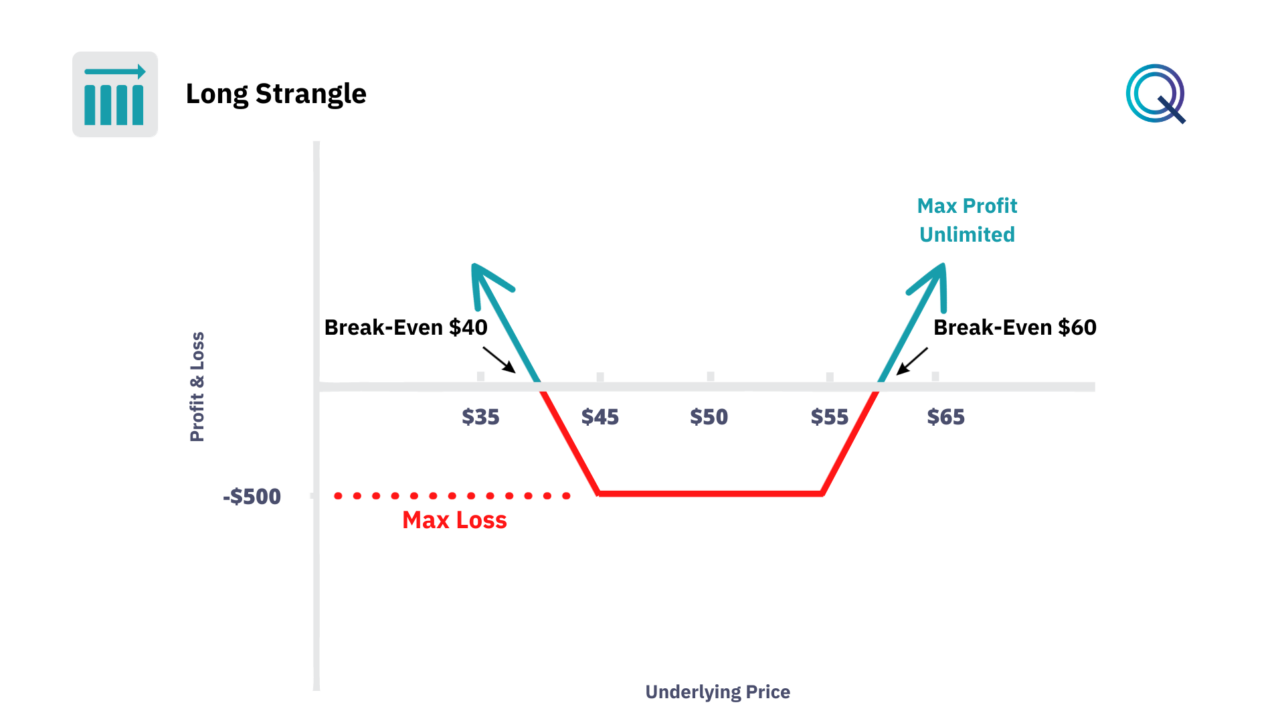

Payoff Diagram of the Long Strangle

Every option strategy has a potential return and a potential maximum loss. These two values can be displayed through the payoff chart. Let’s look at the payoff of the Long Strangle Strategy.

In this example, the stock is quoting at $50, and we buy a call with a $55 strike and a put with a $45 strike at a cost of $5.

- Our maximum loss is $500 ($5 * 100 shares), which is the sum of the two premiums paid.

- The potential profit of the strategy in this case is unlimited.

- The breakeven price is represented by the strike +- the cost of the premium, which is $5. The breakeven points are $40 and $60. The underlying must move below $40 or above $60 to be profitable.

Let’s look at different scenarios:

- If at expiration the price of the underlying is below $40, the trader profits on the put side.

- If at expiration the price of the underlying is above $60, the trader profits on the call side.

Market Scenarios for the Long Strangle

There are various factors we should consider before using a Long Strangle.

- Earnings Reports and Major Announcements. The uncertainty of how a stock will react to earnings or regulatory news can lead to increased volatility. A Long Strangle can capture profits from significant price swings in either direction following such events.

- Economic Data Releases. Major economic indicators, such as employment data or interest rate decisions, can cause widespread market volatility. A Long Strangle can be an excellent strategy to employ in anticipation of these data releases.

- Sector-Specific News. If there is a catalyst that could affect an entire sector, such as a technological breakthrough in biotech or a change in energy policy, a Long Strangle can be used to speculate on the resultant volatility without taking a directional bet.

- Adjusting Strikes and Expirations. Depending on how the underlying asset moves, an investor might adjust the strikes or expiration dates of the options in a Long Strangle. If the stock moves towards one of the strikes, the trader could roll the opposite option closer to the money to collect more premium or extend the trade’s duration.

- Delta Hedging. To manage the directional risk associated with the Long Strangle, traders might implement a delta hedging strategy, adjusting their position to maintain a delta-neutral stance as the market moves.

- Volatility. Since a Long Strangle benefits from an increase in volatility, traders should closely monitor the implied volatility levels. If volatility spikes, they might consider taking profits earlier than planned.

- Cost of the Strategy. While a Long Strangle is cheaper than a Long Straddle, it still requires a significant outlay for the options premiums, which could be lost if the market does not move enough.

- Time Decay. As the expiration date approaches, time decay accelerates, particularly affecting out-of-the-money options. It’s essential to manage the timing of the strategy carefully.

- Liquidity and Bid Ask Spread. The liquidity of the options chosen for a Long Strangle should be considered, as illiquid options can have wide bid-ask spreads, potentially reducing the profitability of the strategy.

- Straddle Conversion. If the movement of the underlying asset makes the strangle less profitable, converting to a Long Straddle by adjusting the strike prices to at-the-money can be a way to respond to decreased volatility.

Conclusion

To recap:

- The Long Strangle Strategy is a Market Neutral strategy

- Our position is Long Options. It is a Debit structure

- The strategy benefits from an increase in volatility

- Time is a negative factor for this strategy

Other Market Neutral Strategies

Here are other neutral strategies with Options: